Prices for flexible packaging materials increased almost across the board in the first quarter of 2026 compared with the previous quarter. Rising energy and raw material costs, combined with escalating geopolitical tensions, continue to impact the markets. The latest figures published by Flexible Packaging Europe (FPE) present a concerning picture across the different substrates. It should be noted, however, that the reported figures reflect the entire first quarter of 2026 and therefore still appear comparatively moderate when set against the more pronounced developments observed in the final weeks of the quarter due to the conflict in the Middle East.

Mixed developments

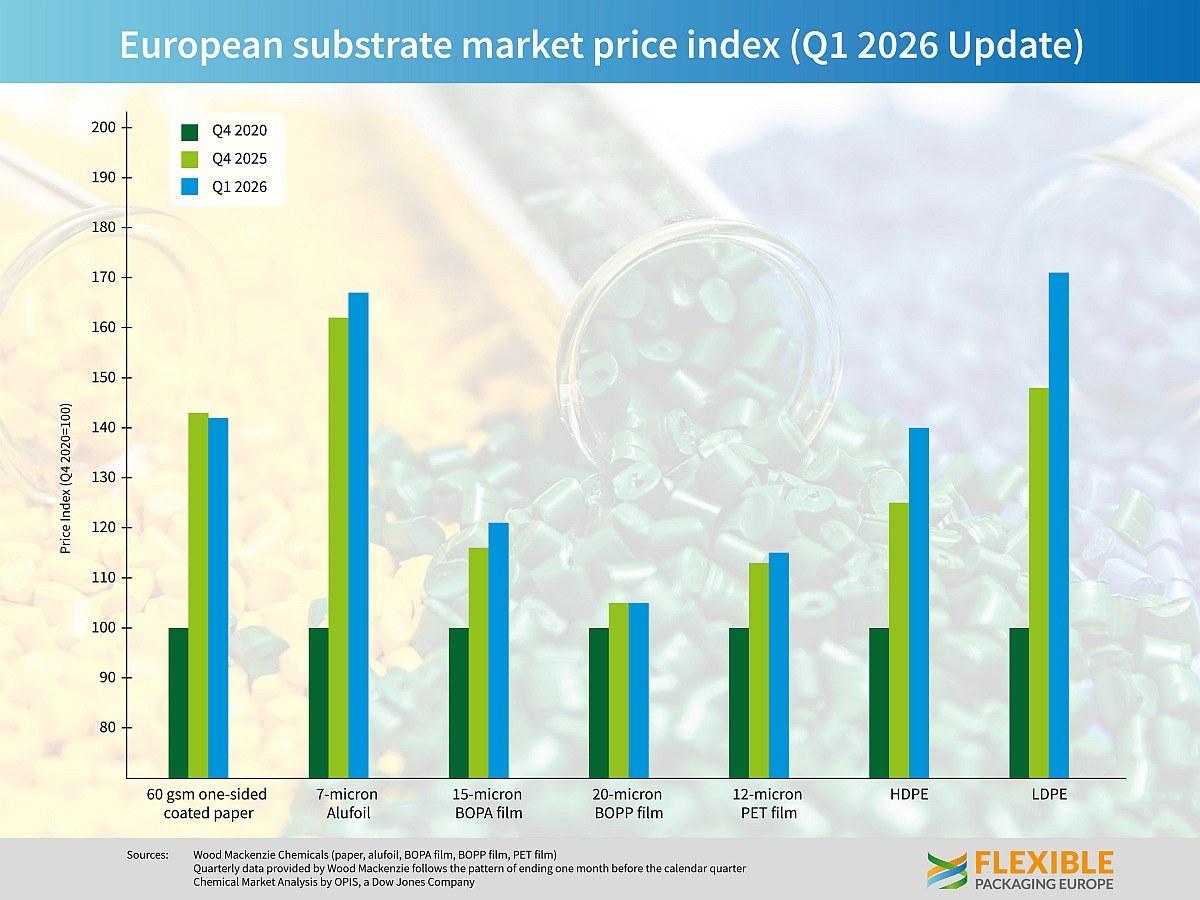

One-side coated paper (60 gsm) recorded a slight decrease of 1% compared with the fourth quarter of 2025, while prices for 7-micron aluminium foil increased by 3%. Plastic films showed a mixed development: BOPA film (15 micron) rose by 4%, while BOPP film (20 micron) remained stable. PET film (12 micron) recorded a moderate increase of 2%. A much stronger trend was observed in polyethylene, with HDPE rising by 12% and LDPE by 16%. At the same time, the polyethylene market remains tight, as rising feedstock and energy costs continue to put pressure on prices.

Alexander Tkachenko of Wood Mackenzie commented: “In Europe, quarterly prices for BOPET films rose alongside a surge in imports. Prices for BOPA film and aluminium foil also climbed, while BOPP prices remained largely stable and paper prices edged down slightly. In contrast, aluminium foil prices advanced, driven by higher LME prices, although conversion costs eased. Due to the US-Iran conflict, obviously, oil prices have risen and expect all substrates to rise in price and be affected. We expect that offshore prices will be affected from March onwards, and for domestically produced film to be affected April onwards. The fact that offshore prices will be affected in two ways: increasing raw material costs and freight, we expect it to go up quickly and materially. This will provide some pricing relief to domestic producers who may see an uptick in demand as local converters may look for security in materials delivered.”

Kaushik Mitra of Chemical Market Analytics by OPIS, a Dow Jones Company, added: “The Iranian crisis has created a significantly high level of uncertainty and volatility in the market. In the first days of the conflict, it seemed as though the impact would be localised in the Strait of Hormuz adjacent areas, but now it is becoming evident that the impact would be very widespread, especially in Asia, because of the dependence on feedstock from the Middle East. Our assessment suggests that the World PE/ PP market will become tighter because a large number of capacities would have to be turned off due to feedstock problems, physical impact and displacement of the supply chain.

Europe is less dependent on the Middle East than Asia

The situation in Europe is slightly different. Independently, from a feedstock point of view, Europe is less dependent on the Middle East than Asia, plus the proximity to the North American resources makes the European raw material situation a bit more stable and supply shocks a bit less likely. But the cost inflation will be significant, already gas prices, which go to utilities, are more than double and naphtha prices are up by 40%. This will cause price pressure. Moreover, to replace Middle East PE/PP volume, European operators will need to run their plants much harder, for which they need a price incentive. The US suppliers can raise exports to Europe, but they have limited surplus capacity, and now that everyone is asking for material, in this situation, they will choose the best netback destinations. In other words, Europe will compete with Asia and other markets where prices are going up strongly as well.

So, overall, looking ahead, prices could face significant inflation and volatility if the situation in the Middle East continues. It is very difficult to say how long the crisis will last, but looking at the damage and dislocation, even if the crisis ends shortly, there will be supply chain bottlenecks and a long repair and rebuild period before normalcy returns. So, it is reasonable to expect significant volatility in the short to medium term and tightness on some raw materials in the European market due to global competition for the resins.”

Guido Aufdenkamp of Flexible Packaging Europe (FPE) commented: “The current developments in raw material markets clearly demonstrate how strongly geopolitical events can influence price developments. Rising energy and raw material costs, but also reduced availability, are creating significant pressure along the entire value chain. The European flexible packaging industry is working intensively to ensure the security of supply to the food and pharmaceutical industries. The coming months are expected to be characterised by continued uncertainty and high volatility.”